Be sure to share these materials with friends, kin, and workmates.

Ben Norton

GER

Geopolitical Economy Report

This video, presented by Ben Norton of the Geopolitical Economy Report, analyzes the escalating conflict between the United States and Iran. Norton argues that what was intended to be a quick, decisive military campaign has devolved into an uncontrollable regional quagmire for the Trump administration (0:00 - 4:00).

This video, presented by Ben Norton of the Geopolitical Economy Report, analyzes the escalating conflict between the United States and Iran. Norton argues that what was intended to be a quick, decisive military campaign has devolved into an uncontrollable regional quagmire for the Trump administration (0:00 - 4:00).

Key takeaways include:

- Failed Diplomatic Efforts: The administration announced a "pause" in fighting on July 25, 2026, but it collapsed after only four days, with airstrikes resuming on July 29 (1:17 - 1:34).

- The Three Drivers of the Crisis: Norton identifies three primary factors forcing the US to seek an off-ramp:

- Missile Shortages: The Pentagon is running dangerously low on Patriotinterceptors, with analysts estimating they have used roughly 60% of their initial inventory since the war began in February 2026 (10:40 - 16:07).

- Rising Casualties: The video claims the Pentagon is hiding the true extent of USmilitary fatalities and injuries to avoid political backlash before upcoming midterm elections (21:02 - 24:26).

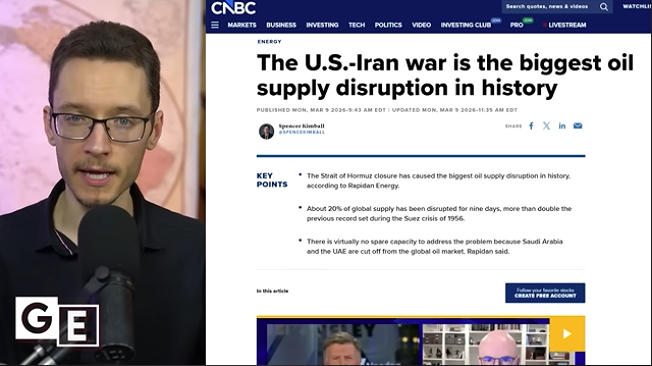

- Energy Crisis: The expansion of the conflict to include Yemen and the subsequent Houthi blockade of Red Sea oil routes—combined with Iran's closure of the Strait of Hormuz—has severely tightened global oil supplies and driven inflation (24:26 - 30:14).

Conclusion: Norton asserts that the US is facing a strategic defeat, claiming that Iran has essentially "won" the conflict. He argues the Trump administration is now in a desperate, contradictory position: seeking to end the war due to mounting logistical and economic failures while simultaneously trying to project a narrative of victory to the American public (5:49 - 6:19, 30:44 - 32:14).